How OBBA New Car Loan Interest Deduction Works

Understanding the New Car Loan Interest Deduction Under the OBBA

The One Big Beautiful Act (OBBA) introduces a new deduction for car loan interest that can be easy to misunderstand or misapply if the requirements aren’t carefully reviewed. While it may sound straightforward, the details around vehicle eligibility, loan structure, and income limits are critical. Missing any one of these rules can result in claiming a deduction that doesn’t actually apply.

Below is a breakdown of how it works, who qualifies, and how it must be reported.

What This Deduction Is

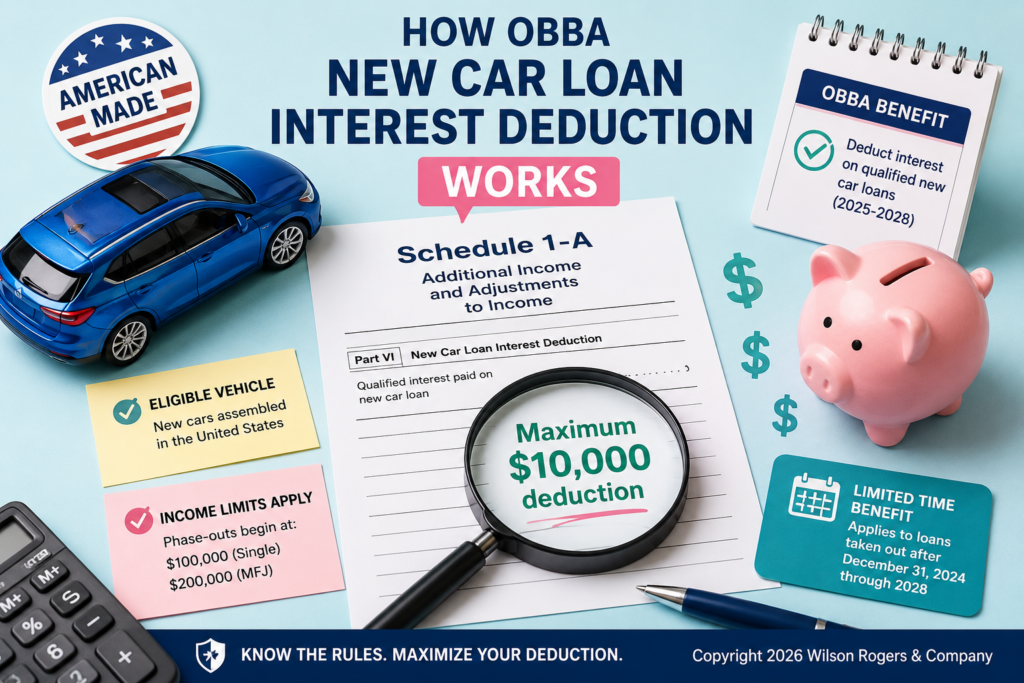

Under the OBBA, taxpayers may deduct interest paid on a qualified passenger vehicle loan. The key distinction here is that only the interest portion of the loan qualifies—not the purchase price, not the down payment, and not any related costs like insurance or registration. Another important feature is how the deduction is claimed. It is available regardless of whether you itemize deductions, which makes it more broadly accessible than many traditional tax breaks. Instead of being reported on Schedule A, it is taken on Schedule 1A, reducing your adjusted gross income directly.

Vehicle Qualification Requirements

This is the most important part of the rule set, and it cannot be overlooked. Before considering any interest amounts, the vehicle must be confirmed as qualifying.

The vehicle must be for personal use and cannot be used for business or mixed-use purposes. It must be a passenger vehicle and must have final assembly occurring in the United States. It also needs to meet IRS passenger vehicle weight limits.

In addition to the vehicle requirements, the loan itself must also qualify. The loan must be incurred after 2024 and must be secured by a first lien, meaning it is a secured loan used specifically to purchase the vehicle. If any of these requirements are not met, the deduction does not apply.

Caps, Phase-Outs, and Reporting

The deduction is capped at $10,000 of interest per tax year. It begins to phase out when adjusted gross income exceeds $100,000 for single filers and $200,000 for married filing jointly. Once income exceeds these thresholds, the available deduction is gradually reduced until it is fully phased out.

How to Report the Deduction

The deduction is calculated and reported on Schedule 1A of Form 1040. This is a deduction, not a credit, meaning it reduces taxable income rather than directly reducing tax liability.

Proper documentation is also required. Taxpayers must have lender interest documentation such as Form 1098-V or a similar statement to support the deduction.

Important Reminder for Business Vehicles

Business vehicle interest follows entirely different rules and must not be combined with this deduction. The OBBA provision applies strictly to qualified personal-use vehicles, and blending business interest into this calculation would result in an incorrect application of the rules.

In Summary

This deduction is temporary and is currently available for tax years 2025 through 2028. Proper application requires careful verification of vehicle eligibility, loan qualifications, adjusted gross income thresholds, and correct reporting on Schedule 1A. While it can provide meaningful tax savings, it is highly dependent on meeting all qualification rules exactly as outlined.

What is Circular 230 & Why Taxpayers Can Feel at Ease

Ever feel nervous handing over your tax documents to someone else? You’re not alone. Every year, taxpayers trust preparers with their most personal financial information—income, investments, dependents, and more—hoping everything is done correctly.

The good news? There’s already a safeguard in place to protect you and hold your preparer accountable. It’s called Circular 230, and it’s one of the most important—but least known—rules in the tax world.

What Exactly is Circular 230?

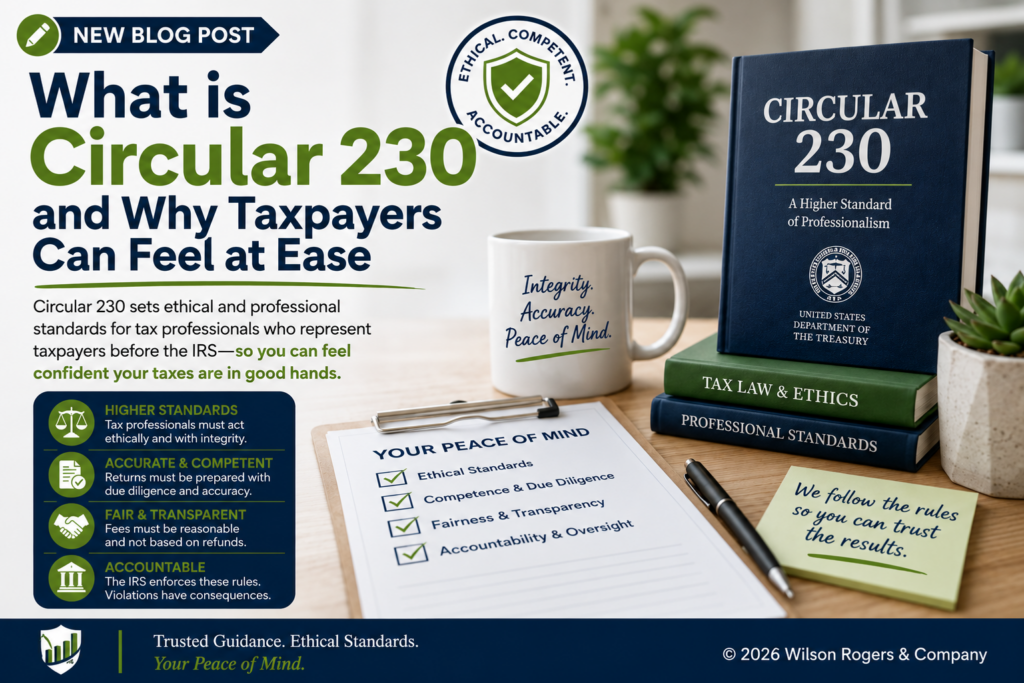

Circular 230 is an official publication from the U.S. Department of the Treasury. It sets the rules and ethical standards for professionals who represent taxpayers before the IRS.

This includes CPAs, Enrolled Agents (EAs), tax attorneys, and other individuals authorized to practice before the IRS. Essentially, if someone is legally allowed to handle your taxes, they must follow Circular 230.

Think of it as the IRS’s code of conduct for tax professionals. It ensures that your preparer acts with integrity, honesty, and professionalism—giving you confidence that your taxes are in capable hands.

How Circular 230 Protects You

Circular 230 exists not just for professionals, but for taxpayers. It ensures that anyone handling your return is competent, ethical, and accountable.

First, it holds preparers to a higher standard. They must act ethically, avoid conflicts of interest, and exercise due diligence. Misleading clients, making unrealistic promises, or taking risky tax positions is not allowed.

Second, it requires accuracy and competence. Tax professionals must verify information and ensure returns are correct. This reduces the risk of errors, penalties, or audits from sloppy or negligent work.

Third, it promotes fairness. Circular 230 regulates fees in many cases, preventing unreasonable or contingent charges. You can trust you’re being charged fairly, not based on the size of your refund.

Finally, it enforces accountability. The IRS Office of Professional Responsibility monitors compliance, and a preparer who acts unethically can be suspended or barred from practice. That oversight means you’re not on your own if something goes wrong.

Why This Matters to You

Working with a preparer covered under Circular 230—like a CPA, EA, or tax attorney—gives you peace of mind. They are legally bound by federal ethics and practice standards, required to act in your best interest, and can face real consequences for misconduct.

Put simply, Circular 230 gives you a safety net every time you file. Your preparer is trained to handle your taxes responsibly, accurately, and ethically.

Your Role as a Taxpayer

Circular 230 protects you, but you still play a key role in keeping your tax process safe. Always confirm your preparer’s credentials, review your return before signing, keep copies of your records, and provide accurate information. Being proactive helps protect both you and your preparer.

Final Thoughts

Most taxpayers never think about Circular 230, but it works quietly in the background to keep the tax system ethical, fair, and accountable. It’s why you can hand over your financial documents to a qualified preparer and trust that they are required to act professionally.

Behind every trusted tax professional is a set of IRS-enforced rules designed to protect you. Circular 230 gives taxpayers peace of mind, knowing their preparer is qualified, ethical, and committed to doing things the right way—every single time.

Benefits of E-Filing vs. Paper Filing

E-Filing vs. Paper Filing: Which Is Better for Taxpayers?

When tax season arrives, one of the first decisions taxpayers face is how to file their return. While paper filing was once the standard, electronic filing—commonly known as e-filing—has become the preferred method for both taxpayers and the IRS. And for good reasons. E-filing offers speed, accuracy, and security that paper simply can’t match.

Whether you file on your own or work with a tax professional, understanding the benefits of e-filing can help you make a confident, informed choice.

Faster Processing Means Faster Refunds

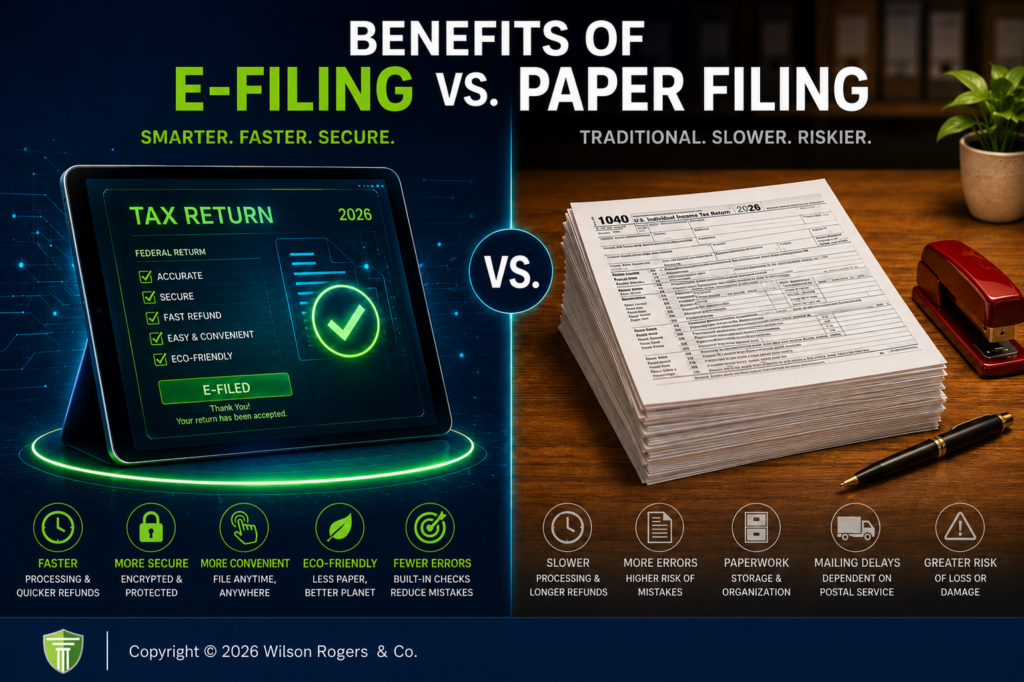

One of the most significant advantages of e-filing is how quickly your return moves through the IRS system. Electronic returns are transmitted instantly and begin processing within hours. In most cases, taxpayers who e-file and choose direct deposit receive their refunds in 1–3 weeks.

Paper returns, on the other hand, must travel through the mail, wait in IRS processing queues, and be manually entered into the system. This often results in 6–12 week wait times—and longer during IRS backlogs.

If getting your refund quickly is a priority, e-filing is the clear winner.

Greater Accuracy and Fewer IRS Notices

E-filing significantly reduces the risk of mathematical errors and missing information. Tax software automatically performs calculations, checks for inconsistencies, and flags required fields before the return is submitted. The IRS reports that e-filed returns have a much lower error rate compared to paper filings.

With paper returns, even a small mistake—such as a mismatched Social Security number or an overlooked signature—can trigger delays or IRS notices.

E-filing helps avoid these issues and ensures your return starts on the right foot.

Immediate Confirmation of Submission

Waiting and wondering whether the IRS received your paper return can be stressful. With e-filing, you receive electronic confirmation that your return has been received and accepted. No guessing, no tracking numbers, and no risk of lost mail.

For taxpayers who value peace of mind, this acknowledgment is a major benefit.

Enhanced Security and Data Protection

E-filing systems use encrypted, secure channels to protect your sensitive financial information – the same level of protection used by major banks. Paper returns, however, can be lost, misdelivered, or even stolen while being mailed.

If safeguarding your personal information is a top priority, e-filing offers the strongest layer of protection.

Easy Access to Prior-Year Tax Documents

When you e-file, your tax professional or software program securely stores your return and supporting documents. If you need a copy for a mortgage, loan application, or audit, retrieving it takes seconds.

Paper returns can be misplaced or damaged, creating stress when documentation is needed most.

Environmentally Friendly

E-filing cuts down on unnecessary paper and reduces waste. It’s a simple way to go greener during tax season.

Required for Many Preparers and Businesses

The IRS requires certain tax preparers and many businesses to electronically file once they meet specific thresholds. E-filing helps ensure compliance and avoids penalties, making it the practical choice for most professionals.

When Paper Filing May Be Necessary

Although e-filing is the preferred method, there are a few situations where paper filing may still be required or beneficial:

- Filing After the E-File Deadline

Once the IRS e-file system shuts down for the season—typically in October—late returns must be submitted on paper. This often happens when taxpayers miss both the regular deadline and any extension deadline.

- Returns That Cannot Be E-Filed

Certain uncommon forms, elections, or specialized filings cannot be submitted electronically. For example, if your return includes forms the IRS does not support for e-file, a paper return may be necessary.

- Correcting Identity or Data Issues

If the IRS rejects an e-filed return due to mismatched Social Security numbers, prior-year AGI problems, or identity theft flags—and the issue can’t be resolved electronically—a paper return may be required.

- Amended Returns (in rare cases)

Although most amended returns can now be e-filed, some older tax years or special situations still require mailing a paper Form 1040-X.

- Filing Without Proper E-File Access

Taxpayers with limited technology access or those who prefer physical signatures in rare circumstances may choose paper filing, though this is far less common.

While these situations exist, they are the exception—not the rule. For the vast majority of taxpayers, e-filing remains the most efficient and reliable option.

Conclusion

While both e-filing and paper filing will get your tax return to the IRS, the benefits of e-filing—faster refunds, fewer errors, stronger security, and immediate confirmation—make it the smarter choice for most taxpayers. Paper filing still plays an important role in special situations, such as filing after the e-file deadline or handling uncommon forms the IRS doesn’t support electronically. But for everyday taxpayers and most businesses, e-filing remains the simplest, safest, and most efficient way to stay compliant during tax season.

Origins – The History of xXx Racing

xXx Racing – Athletico Racing Since 1999

Many people who know me, may be familiar with the fact that I race bikes for a team called xXx Racing – Athletico. The team was founded back in 1999 by a group of messengers, but just who exactly were these individuals? Where did they come from and what prompted them to form the team? As the team has grown and membership has changed over the years, some of the nuances and details have become lost to the sands of time. With the team approaching it’s 25th Anniversary, this story pieces some of that “lost history” back together for all to witness and revel in for years to come.

Me at Cherry Roubaix Crit, Traverse City, MI Cir. 2013

Now a special note about this post. I’ve been on xXx, commonly referred to as “Triple X” since 2007. Back in 2012 I did a lot of the research that appears in this post between the team’s 10th and 15th Anniversaries. I had the opportunity to speak with Marcus (see below) on several occasions as I wanted to get the details correct. But as time has passed, a lot of the internet links that contained that history have since been broken or deleted. To that end, this post contains links and PDF files of those same links so that if they are broken in the future, readers will still be able to enjoy and find the original content. If there is a file with the content, it’s denoted with (PDF) to alert you to it. Now with that said, let’s get to the story!

The Beginning

It all began with a guy by the name of Marcus Moore. Marcus worked as a bike messenger in downtown Chicago up until 1995 when he then started working as a mechanic. In 1997 he founded Yojimbo’s Garage, a local bike shop, (PDF) after splitting time between being a carpenter and working at Upgrade Cycles.

Marcus Moore, xXx Racing Founder and owner of Yojimbo’s Garage

As Marcus was into the racing scene as well as that of messengering here in Chicago, he sponsored a single rider in 1997 at our local track, the Northbrook Velodrome. However, the rider burned out and didn’t go back the following season. In 1998, one of his fellow messenger friends, Patrick Babcock, decided to try his hand at track racing. It took Patrick about three or four times to get comfortable with the style of racing, but then he got hooked.

My track number, still being sponsored by Yojimbo’s Garage!

Patrick got wind of a race that was being held in Toronto Canada in October of 1998 and wanted Marcus to go. The race? One of those crazy Alley Cat Scrambles on the Human Powered Roller Coaster track (PDF). This track saw messengers come from all over the world to compete in events such as the Cycle World Messenger Championships. Marcus and Patrick really liked the messenger scene and the vibe they got about racing. There were some organized teams; some that even had women. During the ride back to Chicago, Marcus and Patrick wondered if other messengers might also have an interest in racing. They also talked about forming a race team.

Messenger racing at The Human Powered Roller Coaster

In late 1998 Marcus founded the Alley Cat series called the “Tour Da Chicago” (PDF), which was a muti-race series that was run over a period of time and held on the city streets. It wasn’t necessarily “sanctioned” racing, but it was “organized” and allowed messengers and other strong men/women to prove their mettle and show who was the baddest on two wheels. In November, Marcus and Patrick called a meeting among the messenger community to see to what extent their desire to race actually was. The result? 28 people showed up, which was a very promising turnout. At another meeting, the group sifted through more than 40 suggested names for the team, finally settling on xXx. The name wasn’t inspired by anything of a racy nature, but by a Toronto restaurant named the xXx Cafe that Moore liked and he and Patrick had eaten at during their trip. With that, the foundation had been laid for the team to start racing in 1999.

Team Colors

During that winter of 1998 – 1999, they filled out the paperwork to formally launch the team. It was also during this period that the team settled on our team colors of red, black and white. The history of this is that the colors came from the historic Chicago colors (PDF) of the anarchist movement and uprisings in the early 1900s (PDF) and the fact that they were edgy. Most of the other teams at that time were rather “traditional” whereas the founders of xXx wanted to push the envelope and prove a point. You didn’t have to have a fancy bike and all that gear to be fast or win races. Messengers are fast too and we’re about to show Chicago how we can throw down!

Racing Since 1999

In its earliest incarnation, xXx served primarily as a support system for couriers, but the team made a conscious decision not to restrict its membership, and soon attracted racers of all stripes. While this is in no means an exhaustive list, here are some of those riders who made up the founding/initial team with the years for which results listing xXx Racing can be found:

Marcus Moore (’99), Patrick Babcock (’99), Mike Genge (’99), Eric Sprattling (’99), Thomas McBride (’99), Jason Pyrzynski (’99), Donny “Quixote” Perry (’00), Jeff Benjamin (’00) Zach Fiocca (‘99), Sarah Tillotson (’01), Lissa Krawczyk (’01)

The exact date of when the team was founded isn’t necessarily known but the first race that included results with a majority of the founding riders was the Parkside Criterium Number 3 that was held in Kenosha Wisconsin on April 11, 1999. Back then there was no Cat 5 so most of the riders were in the “Senior 4” category…with the exception of Eric Sprattling.

Team Mentoring

Each one of the riders above brought something unique to the table. All had a love for the bike and going fast. However, there was one rider who brought a little something extra with them; the gift and desire of mentorship. Eric Sprattling rode as a messenger for 13 years. One of the companies he rode for was named Deadline Express. He was also into the Alley Cat racing scene as well as that of sanctioned racing; Eric actually rode for the True Value team of the ‘90s before he helped with the foundation of xXx. With that being said, Eric had a good idea of how racing worked. He also knew that it took training to be any good at it.

Eric Sprattling rockin his True Value race jersey!

Rumor has it that Eric would bump into other messengers during the week and would ask them what they were doing on Saturday. When the respondent replied, Eric would say “Wanna Go For A Ride?” or something along those lines. Early on Saturday morning, Eric would ride to one guys house and meet up with them. The two riders would go to the next guys house and repeat the process until they had a caravan of riders. They would then all traipse up to the northern suburbs (e.g. Highland Park, Fort Sheridan) and sometimes even farther. It was this mentorship that afforded these messengers and friends a route into structured training and racing. Fellow teammate Kyle Wiberg recounts (PDF) how Eric dragged him out to a bike race being held in Sherman Park back in 1989. Eric would later join Kyle at the messenger company Kyle founded back in 1989, Velocity.

Aside from being a mentor, Eric was also an inspiration to these riders. When xXx was founded, Eric was already in his 40’s. As some put it, he was winding down his racing career and wanted to pass on what he knew to others. But while he may have been winding down, he certainly wasn’t being a slouch. You see, stories have it that Eric was one heck of an endurance rider. Many accounts point to the fact that he participated in 6 and 12 hour time trials on more than one occasion. These events were held somewhere around the Charles Mound Illinois area. In preparation for these events, Eric often rode long distances as part of his training. One account mentions that Eric rode from Chicago to Wisconsin, raced his bike and then rode back home. It was also known that he would ride to the Wisconsin and Indiana boarders all within the same day. An account of Eric’s racing prowess appeared in Chapter 9 “Alley Cat” (PDF) of Travis Culley’s book The Immortal Class.

Side note – I rode as a messenger between 1995-1997 during the Summers of my Senior Year in high school and the one leading into my Junior year in college. I was #512 of the “now defunct” Chicago Messenger Service. Now, I do not have a great memory of who ALL the messengers were during that time because I was a kid. But it is literally quite possible that I could have bumped into Eric during those years. If it did happen, I chalk it up to fate that I would later ride on the same team that he founded!

Tragic Moments

While 1999 remains a focal point in our founding, it was one of three very challenging years for our team. Tommy McBride was one of the early messengers who joined the team. As a young chap, he worked at Arrow Messenger in 1996 and later helped found On The Fly Courier. Unfortunately, Tommy’s life was cut short when he was killed in a road rage incident at 5300 W. Washington on April 26, 1999. A memorial dedicated to Tommy can be found on the bicycle messenger memorial page (PDF).

That same year, just a few short weeks later, Eric suffered a brain aneurysm during the Circuit of Sauk (aka Baraboo) road race in Wisconsin. Unfortunately he would not recover and passed away on May 7, 1999. A memorial dedicated to Eric can be found on the same bicycle messenger memorial page (PDF).

McBride and Sprattling were memorialized in the 13th issue of “Dead Air,” the messenger zine edited by Donny “Quixote” Perry (former leader of the Windy City Bike Messenger Association).

In 2007, the year I joined the team, we were unfortunate to suffer two other tragic losses.

Elizabeth “Beth” Kobeszka

Elizabeth “Beth” Kobeszka, was an avid triathlete and joined xXx and began competing in bike races throughout the region. On June 30, 2007, at the age of 24, Beth was killed in a biking accident during the 20th Annual Proctor Cycling Classic in Peoria, Illinois. Continuing her lifelong legacy (PDF) of helping others, Beth was an organ donor.

Pieter Ombregt

Pieter Ombregt was a member of xXx Racing-Athletico for two seasons from 2006-2007. He was a gifted photographer, an accomplished cyclist and a dear friend to the Chicago cycling community. Pieter died at the age of 27 (PDF) on September 11, 2007, from injuries he sustained in a bicycle racing accident.

Richard Moellering

In 2018, the team suffered our most recent loss with the passing of Richard Moellering. A member of xXx since 2012, Richard embodied the spirit and mission of xXx both on and off the bike. I know many of us strive to be even half as engaged, adventurous, and active as him when we’re in our 70’s. Richard passed (PDF) on April 20, 2018 of complications from a cycling accident.

In honor of all our fallen riders, we wear their hearts on our sleeves as a constant inward and outward reminder that their lives will never be forgotten.

Traditions & Legacies

Over the years, many things that became common place within xXx Racing actually had their origins with the people and places surrounding the events in 1998/1999.

As mentioned earlier, the team began with the focus of mentoring couriers as they began sanctioned racing. As early as June 19, 1999, (PDF) riders were venturing up to the Northbrook Velodrome to participate in track races under the xXx Racing banner. This attracted other non-messengers who wanted to race; none of which were ever turned away. It was this open door policy that started the practice of xXx racing being a team open to all. To this day, we remain one of the principle conduits within Chicagoland for new racers to enter into the sport. Additionally, xXx maintains an active and accomplished presence at the Northbrook Velodrome.

In 2001 Randy Warren joined the team in a coaching capacity. This move filled the role started by Eric with regards to someone being able to provide advice and knowledge with regards to training and racing. It was also during this time that the team began working closely with the Active Transportation Alliance and other cycling organizations to help promote cycling in the community.

Athletico Physical Therapy joined xXx Racing as a sponsor in 2002 and became our co-title sponsor in 2003, creating the xXx Racing-Athletico team. We are thrilled to be partnered with Chicago’s finest source of physical therapy and sports medicine.

With regards to us being a development team, various programs focused on fostering this aspect began to emerge over time. The current Men’s Development Program (MDP), Women’s Development Program (WDP), Junior Development Program (JDP) and Elite Development Program (EDP) all have their roots in the concept of nurturing and growing our riders. In 2006/2007, one of those programs was the Messenger Program, which was a historic nod back to our roots.

Our team ride that leaves Wicker Park and heads up to the northern suburbs, follows popular routes that are used by many North Shore cyclist. However, Eric was using these routes back in the late ‘80s and early ‘90s for his own training and that of his messenger colleagues. Maybe it’s no coincidence that we still venture that way to this day on our Saturday Team Ride. And on a related topic, in 2010 Coach Warren started the 3 States Memorial Ride as a nod to Eric and some of the epic training that was attributed to him. Back in 2012, as a personal nod to Eric I rode to all 4 of our surrounding states (Illinois, Indiana, Michigan and Wisconsin) in a single day. You can read about it in “200+ Miles & 4 States on A Bicycle” which is here on our blog.

For years, xXx held the Sherman Park Race at the location which bears this moniker. In fact, the park is one of the few in Chicago, that has a roadway in it that was actually designed to be used for leisurely activities, like bike riding, back in the early 1900’s. The inaugural race (of recent times) according to the Chicago Tribune was held by the Chicago Park District in 1989. As mentioned above, both Eric and Kyle were in attendance. xXx began hosting the race sometime later and ran it annually through 2011. In 2012 we shifted the venue up north to Lincoln Park, but remain committed to introducing bike racing to those within the city limits.

Notable Championships

With a rich and deep history of riders throughout the years, the team has had several win championship medals and titles. Below is a list of some of the archived and recorded championships. I am sure that there are more that may be undocumented and were lost to the sands of time.

World Championship Medals

- 2010: Greta Neimanas (bronze, Paralympic time trial)

- 2009: Greta Neimanas (silver, Paralympic time trial; silver, Paralympic road race)

- 2007: Greta Neimanas (bronze, Paralympic time trial)

- 2004: Rebecca Much (silver, juniors time trial)

USA Cyling National Champions

- 2016: Steve Burton (masters 60-64 scratch)

- 2016: Johnny Khufahl (juniors 17-18 individual pursuit)

- 2015: Nikos Hessert (juniors 17-18 scratch, team pursuit)

- 2015: Johnny Khufahl (juniors 17-18 team pursuit)

- 2014: Nikos Hessert (juniors 17-18 points, team pursuit)

- 2010: John Tomlinson (juniors 17-18 points)

- 2010: Greta Neimanas (paralympic road race, criterium, time trial)

- 2009: John Tomlinson (juniors 17-18 scratch)

- 2006: Aaron Harrison (juniors 10-12 omnium)

- 2005: Randy Warren (masters 40-44 points race)

- 2004: Rebecca Much (juniors 17-18 time trial)

- 2004: Rebecca Much (juniors 17-18 road race

USA Cyling State Champions

- 2017

- Jake Buescher (cat 1 criterium, team pursuit)

- Courtney O’Neill (team pursuit, individual pursuit, points)

- Tyler George (kilo, individual pursuit, team pursuit, match sprint, Roger Delanghe Trophy Race)

- Solomon Triester (team pursuit)

- Katie George (team pursuit)

- 2016

- Erika Kondo (cat 3 road race, criterium, 500M, scratch)

- Emily Laflamme, Katie George, Erika Kondo, Courtney O’Neill (team pursuit)

- Johnny Khufahl (Cat 1/2 Madison)

- Sean Metz (Cat P/1/2 Road Race)

- Andrei Cismas (junior 15-18 road race)

- Steve Burton (Cat 3/4 Madison)

- Tyler George (Cat 1/2 time trial, Madison, 1000M, team pursuit, individual pursuit, team sprint)

- 2015

- Daryus Patel (juniors 15-18 criterium)

- Courtney O’Neill (Cat 3 criterium)

- Erika Kondo (Cat 4 criterium)

- Emily Laflamme (Cat 4 road race)

- Ryan O’Boyle (Cat P/1/2 road race)

- Tracy Dangott, Michael Kirby (Cat 3/4 Madison)

- Tracy Dangott (Cat 4 Keirin)

- 2014

- Nikos Hessert (Cat P/1/2 points)

- Alec Dinerstein (Cat 3 points)

- Tyler George, Nikos Hessert (Cat P/1/2 Madison)

- Michael Kirby, Rob Whittier (Cat 3/4 Madison)

- Sue Wellinghoff (time trial)

- Tom Briney, Jake Buescher, Tyler George, Randy Warren (team pursuit)

- Alec Dinerstein (Cat 3 scratch)

- Tyler George (4k pursuit)

- 2013

- Nikos Hessert (junior 15-16 omnium)

- WilliamPankonin (35+ road race)

- Sue Wellinghoff (Cat 3 road race)

- Fred Schuler (50+ criterium)

- 2012

- Brenda Culver (Cat 3 mountain bike)

- Mark Baranowski (Cat 3 40-49 mountain bike)

- Ben O’Malley (juniors 15-18 time trial)

- Sandra Samman (3K pursuit)

- Kyle Mindick (juniors 17-18 omnium)

- Tristan Whitehead (Cat 4 criterium)

- Sue Wellinghoff (Cat 4 criterium)

- Daryus Patel (juniors 10-14 criterium)

- 2011

- John Stainthorp (60+ cyclocross)

- William Pankonin (Cat 3 cyclocross)

- Larry Stoegbauer, with help from Jason Garner (Madison)

- Liam Donoghue (individual pursuit)

- Dave Moyer, Liam Donoghue and Larry Stoegbauer, with help from John Tomlinson (team pursuit)

- Dave Moyer (points)

- Ryan Fay (Cat 3 criterium)

- Ryan Fay (Cat 3 time trial)

- Nikos Hessert (juniors 10-14 criterium)

- Dave Moyer (Cat 1 criterium)

- 2010

- Mike Seguin (Cat 3 cyclocross)

- Liam Donoghue (scratch)

- Liam Donoghue, Dave Moyer, John Tomlinson, Randy Warren (team pursuit)

- Dave Moyer (Cat P/1/2 criterium)

- Heidi Sarna (women’s open criterium)

- Samuele Bianchi (juniors 10-14 criterium)

- 2009

- Seth Meyer (Cat P/1/2 road race)

- Dave Moyer, John Tomlinson, Randy Warren, Shane Winn (team pursuit)

- Dave Moyer (points)

- Liam Donoghue (Cat 4 criterium)

- Mike Seguin (Cat 4 30+ criterium)

- 2008

- John Tomlinson (juniors cyclocross)

- Eileen Neville (Cat 4 cyclocross)

- Cecile Redoble (Cat 4 time trial)

- 2007

- Peter Allen (30-34 time trial)

- Joe Ebenroth (Cat 4 30+ criterium)

- Andy Harrison (juniors 10-12 omnium)

- Kevin Krakovsky (Cat 4 30+ road)

- John Tomlinson (juniors 15-18 omnium)

- Jeff Wat (Cat 4 criterium)

- 2006

- Greta Neimanas (juniors 15-18 omnium)

- Ben Popper (Cat 4 cyclocross)

- Janet Lin (Cat 4 criterium)

- Eve Pytel (500M)

- Eve Pytel (3K pursuit)

- Eve Pytel (masters 30-39 500M)

- Eve Pytel (masters 30-39 pursuit)

- John Tomlinson (juniors 10-14 omnium)

- 2005

- Anita Dilles (500M)

- Anita Dillles, Jennifer Hoover, Susan Peithman, Eve Pytel (team pursuit)

- Anita Dilles, Susan Peithman, Eve Pytel (team sprint)

- Emily Macdonald (C cyclocross)

- 2004

- Eric Weisenburger (B cyclocross)

- 2003

- Heather Calomese, Rebecca Much, Brianna Nichols, Eve Pytel (team pursuit)

- Heather Calomese, Brianna Nichols, Eve Pytel (team sprint)

- Sean Hopkins (juniors pursuit)

- Sean Hopkins, Matt Kaminecki, Justyn Moore, William Chotes (juniors team pursuit)

- Sean Hopkins, Matt Kaminecki, William Chotes (juniors team sprint)

- Rebecca Much (200M time trial)

- Randy Warren (points race)

As I bring this history lesson to a conclusion, I want to thank the many people who took the time with me back in 2012 to share all of it with me. I won’t name them here, because many of them are mentioned above. But there were also several sites and articles that contained data that were also used to piece things together. If you want to learn more about the late 90’s messenger or cycling community, or some of the other events that took place around that time, then make sure you check out some of these other articles, which are linked below.

Jared R. Rogers, CPA

xXx Racing – Athletico

Racing 2007 – present

Unofficial “Current” Historian

Other Notable Reads

- xXx racing results from the 2000 season at Northbrook Velodrome (PDF)

- Cycling in Chicago book by xXx Racing teammate Chris McAuliffe (Amazon)

- 90’s Bike Messengering in Chicago Video – Concrete Rodeo

- Bike History in Chicago at YoJimbo’s Garage (PDF)

- John Greenfield – Former Editor of Dead Air (PDF)

- Shoot The Messenger (by John Greenfield) mentions Cully’s book and talks about the death of McBride (PDF)

- Wrong Message (by Kris Darlington Former On The Fly Courier 301) is the editorial retort to Shoot The Messenger and explains why there was so much critical backlash about it (PDF).

- xXx Racing – Athletico bike racing pics from the team Flickr account

- Random bike racing pics Jared has in his old Flickr account

Our FREE Monthly Tax Debt Webinar

Join us for our FREE Webinar!

Tax relief companies advertise help for taxpayers in distress — in exchange for an upfront fee, which can be thousands of dollars. They say they’ll apply for IRS hardship programs to lower or even eliminate your federal tax debts. They even promise to stop back-tax collection. But the truth is that most taxpayers are unlikely to qualify for the programs these scammers advertise.

Upon sign up, you will immediately receive instructions on how to join to the webinar, as well as Jared’s special report “5 Questions To Ask Any Tax Resolution Firm BEFORE Paying Them A Dime.”

To learn more visit www.solvemytaxmess.com and then sign up. Space is always limited so don’t miss your chance to attend this exclusive event!

Click above to watch our Money Management and Tax Chit Chat video series!

Click Above For Your Top Secret Guide To Tax Reduction, Business Success and Solving IRS Debt Problems!

Click Above To Learn 111 Ways To Slash Your Tax Bill!