New Website – Make My Money Make Sense!

We know we’ve been “ghost” for a little while and all we can say is that a lot has happened during the period that we were all dealing with Covid-19. Part of what happened is we were in the Bat Cave deep in work. So today we have two VERY special announcements to make.

ANNOUNCEMENT #1 – The launch of Make My Money Make Sense

We’re very pleased to announce the launch of Make My Money Make Sense – our new financial education and money management website!

This site has been in “development” for a little over 2 years and is the culmination of all those YouTube videos we’ve created. 😁It talks about all things money management for businesses and individuals via our blog, videos and course page.

While it’s being rolled out with a small amount of content, look for it to quickly grow as we finalize some things in the very near future.

A few quick links to check out:

• Website

• Blog article explaining the site and related video explaining George Floyd’s inspiration of this endeavor (we bypassed the beginning of the video so it starts right at the point where Jared tells the story of creating the YouTube channel – which ultimately was being done to roll videos into this site upon completion).

ANNOUNCEMENT #2 – The launch of our first online course

With the launch of Make My Money Make Sense – comes the launch of our first online course! How to File Back Taxes – A Step By Step Guide is now available for purchase. This course is an expansion of our most viewed YouTube video How To File Back Tax Returns | TCC and will teach:

- Those who have back taxes and are looking for a course how to solve them via a DIY method or,

- Tax professionals who want to learn the nuances of filing back tax returns so they can either solve their client’s problems OR learn how to add this valuable service offering to their product line up.

To celebrate, from now until 11:30PM CST on December 31st 2022, customers can get it for 50% off the $97 normal price. To claim the discount use the coupon code “HOLIDAY50” at checkout (case sensitive). If you have any issues using the code just contact us via the email or phone number in the footer of this post.

To purchase the course or learn more you can visit the course and products page on the website or go straight to the sales page.

That’s all for now. Look for us to get back to creating blog content on a more “regular” basis in the very near future!

500 Subscriber Thank You Giveaway

So back when we started our YouTube channel in 2020, we had a goal of getting to 500 subscribers by June of 2021. Well, while we didn’t get there by June, we’re pleased to say that we reached 500 subscribers on August 5th 2021 thanks to your help!

So…thank you, thank you, thank you so VERY MUCH to everyone for helping us reach more people to help them with understanding their money and achieving their wealth goals. But now, we’ve got a new goal, and that goal is to get to 750 subscribers by December 31st 2021. To do that, we’ve got a really awesome contest that everyone can enter whether they are or aren’t a current subscriber of our channel.

Contest Instructions

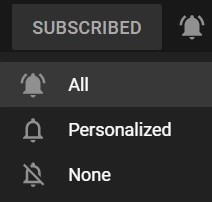

If you’re not subscribed to the channel, all you have to do is just head on over to our channel page. Once there, click the little subscribe button and then make sure you click that little bell icon so it turns grey. That way, you’ll get notifications whenever we upload a new video.

Once you’ve done that, just take a picture or screenshot of your subscription page and shoot it to us via and email by clicking this link. It’s just that simple!

Now if you’re already subscribed, you can still play along and win too. All you have to do is just send an email to some of your closest friends or colleagues inviting them to subscribe to the channel. We put a sample email in the description of this YouTube video to make it really easy for you to just cut paste and send.

Once you’ve sent the email, just either send us a picture of that email or you can actually just BCC us on the email when it goes out. Now don’t worry, we’re not gonna take your friend’s email addresses and spam people or anything like that. ? In the end, you can do whatever your comfortable with. All we need is proof that you’re telling people about the channel.

The Prize?

So what’s the prize? We’ll on Labor Day (9/6/21) we’ll pick 5 lucky winners who will receive a 100% FREE autographed copy of Jared’s book How To Slash Your Taxes Legally and Ethically. Hey, what better way to work on minding your money then by learning how you can save on your taxes for FREE right?

Once again, we thank you all so much for helping us get to our 500 subscriber goal and here’s to us getting to 750 by December 31st.

Money Management YouTube Series

Many Americans often find themselves broke and living paycheck to paycheck. But why does this happen? Is it because of lack of income/earnings? Is it due to not having certain “higher” level education or degrees like a Bachelor’s or Master’s degree from college? Is it because of certain race, gender, sexual preference or other items which can be discriminated against? Contrary to popular belief, it’s NOT just tied to how much money a person makes.

George Floyd’s Impact, Inspiration and Legacy

In early 2020, because of the tragic murder and death of George Floyd, Americans were forced to confront some realities that some would rather not. His death, on top of many Americans being out of work due to the Covid-19 Pandemic, was just enough to push us into a tailspin of social unrest. The resulting looting, rioting and “every person for themselves” mentality which followed, made one thing clear (if it was to no one other than ourselves). Through no fault of their own, many Americans are only one paycheck away from disaster.

This can be a small disaster like missing a cell phone bill, a cable bill or not having enough to go out and eat at your favorite restaurant. Or it could be a serious disaster like missing a rent or mortgage payment, getting evicted, or having to turn to a food pantry for help.

Our good friend, and client, Ashanti Johnson over at 360 Mind Body Soul here in Chicago, encouraged us to start a video series in connection with a virtual wellness summit that our CEO, Jared Rogers, participated in. Check out this specific point in Episode 10 where Jared shares a snippet of her summit and talks about George Floyd and the resulting motivation to launch the series.

In the end, seeing as we deal with money on a day-in and day-out basis, it only made sense that we should work to share the knowledge we have built up over the years with those who need it the most. So, through a culmination of all of the above, we decided that we had an obligation to do more.

Minding My Money Mondays & Tax Chit Chat

Minding My Money Mondays (#MMMM) was the YouTube series that was directly birthed following the events after Mr. Floyd’s death. In early December, we created a separate series called Tax Chit Chat (#TCC) that is for those looking specifically for just tax tips. All videos will ultimately get rolled into a much larger money management website (hopefully by early H2 of 2021), but in the interim, you can follow both series by subscribing to our YouTube channel. Each series has it’s own playlist and releases videos according to it’s prescribed schedule.

Video Episode Listing

Shown below is a listing of the episodes that were created through the date of this blog post. They go from most recent back to the very first episode. To catch an episode, simply click the title above the video thumbnail and you’ll be taken directly to it within YouTube. It’s our sincere hope that that you:

- Enjoy the videos and learn from them

- Spread the word on social media via the hashtags #MMMM and #TCC as we really hope to help people “Make My Money Make Sense!”

- Eventually join us on the money management website once it’s launched

- Send us questions and video suggestions at questions@makemymoneymakesense.com as we hope to help everyone learn how to better manage their money and avoid financial disaster (although NO ONE saw a Covid-19 type event coming).

3 Reasons People Are Broke! | MMMM S1 EP26

Top Year End Tax Saving Tips For 2020 | TCC S1 EP1

How Much To Contribute To Your 401K or Retirement Plan? | MMMM S1 EP25

How to save money buying a new car | MMMM S1 EP24

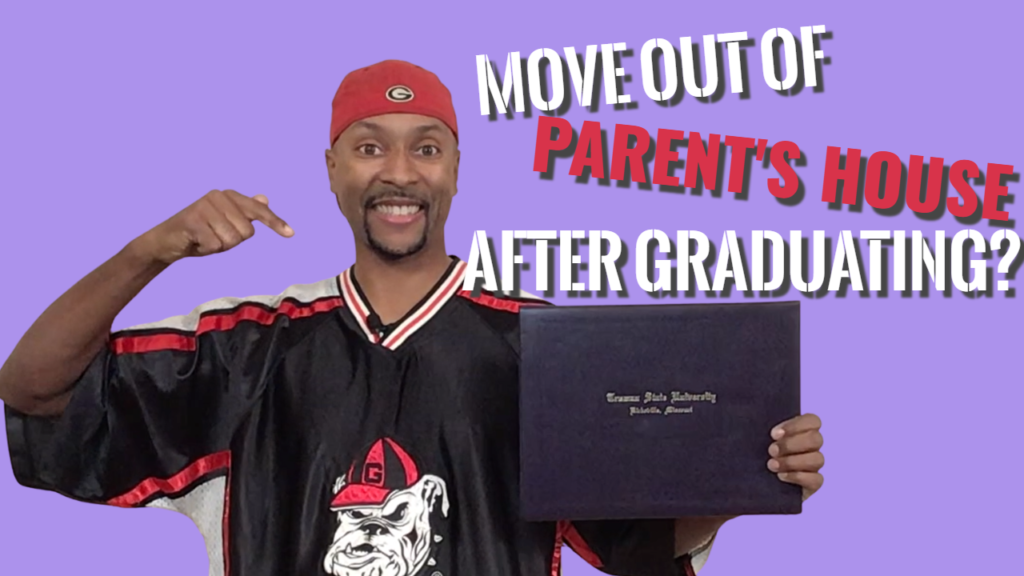

Move Out of Parents House After Graduating? | MMMM S1 EP23

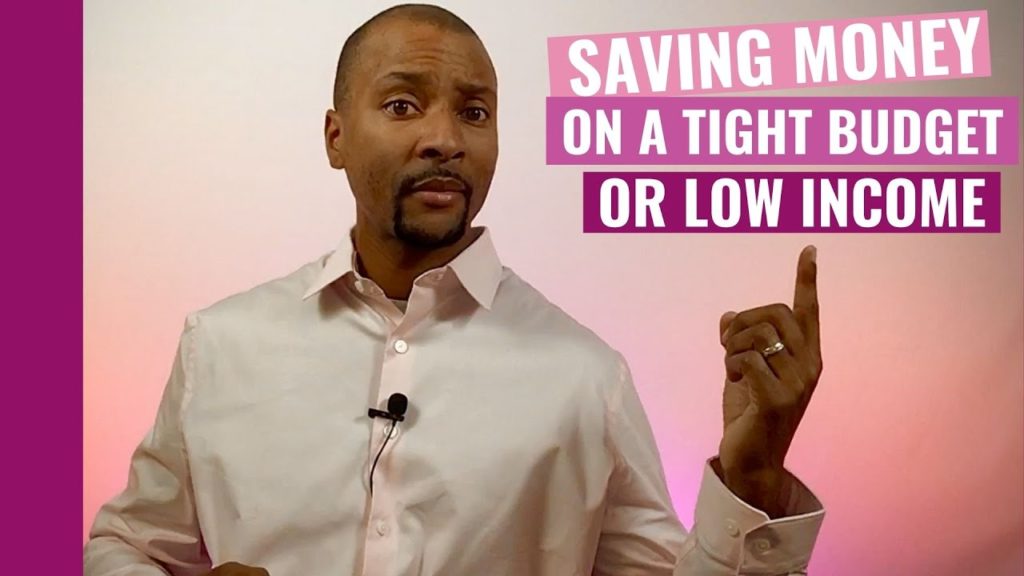

Saving Money On A Tight Budget or Low Income| MMMM S1 EP22

Inherited $200K; Dealing With A Windfall| MMMM S1 EP21

Drain My Savings To Pay Off Debt? | MMMM S1 EP20

Wealth Is A Game of Emotions! | MMMM S1 EP19

Big Bank vs. Online Bank vs. Credit Union | MMMM S1 EP18

Tax Loss Harvesting Explained | MMMM S1 EP16

Student Loans: Pay Off or Pay For Life? | MMMM S1 EP15

Pay Off High Interest of High Balance Card First? | MMMM S1 EP14

Alternatives to low interest CDs | MMMM S1 EP13

5 ways to make $1,000! | MMMM S1 EP12

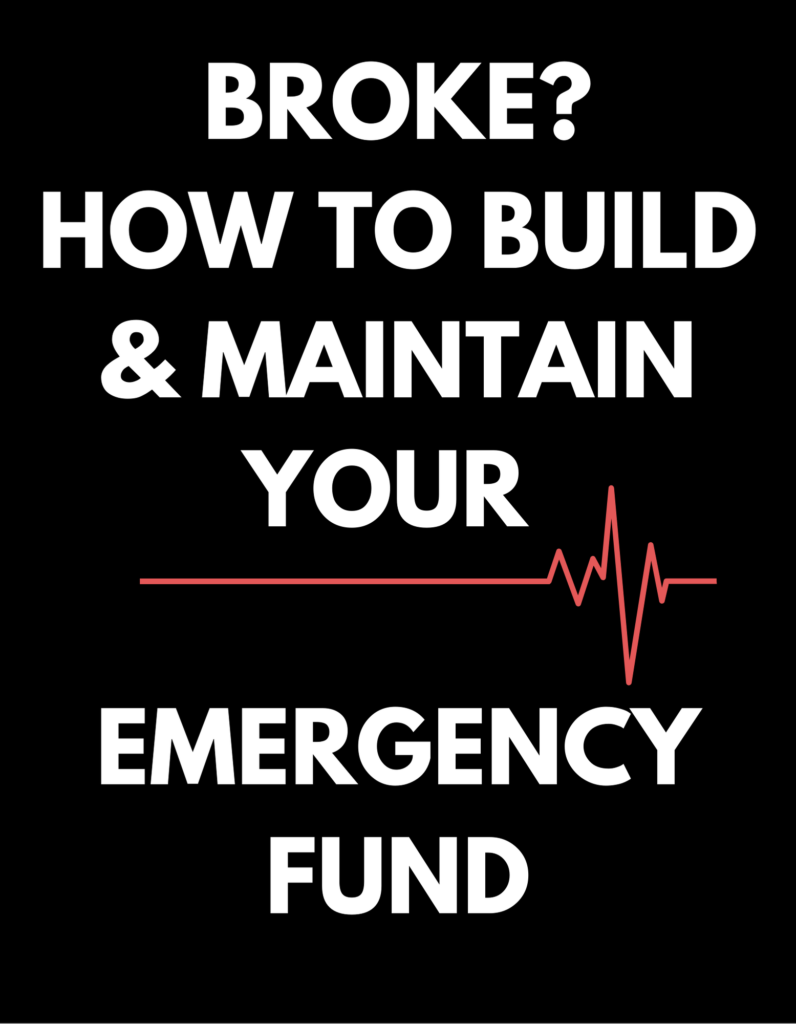

Broke? How to start an emergency fund from ZERO! | MMMM S1 EP11

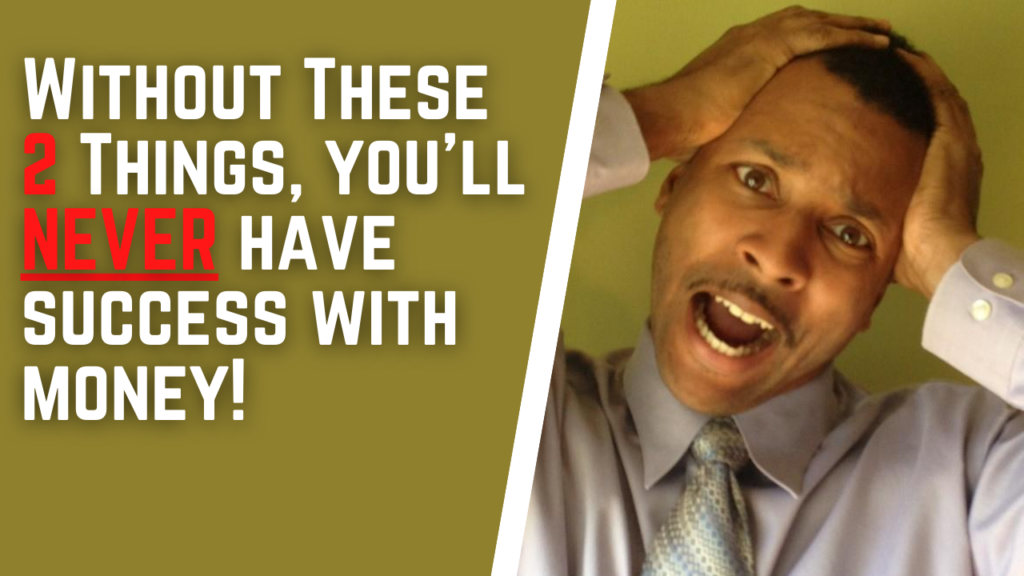

Without these 2, you’ll never have money success! | MMMM S1 EP10

Poor money habits = profits for banks! | MMMM S1 EP9

Rockefeller on The Power of Interest | MMMM S1 EP8

IRS Guaranteed Installment Agreement | MMMM S1 EP7

I Can’t Pay The IRS; Now What? | MMMM S1 EP6

How To Get A 800+ Credit Score | MMMM S1 EP5

What Makes Up Your Credit Score? | MMMM S1 EP4

How Should You Manage Money? | MMMM S1 EP3

What Is A (Ideal) Budget? | MMMM S1 EP2

What is Money? | MMMM S1 EP1

What Happens To IRS Debt When You Die?

Are you wondering what happens to the tax debt of a loved one after their death? Unfortunately, any outstanding amount owed isn’t “automatically” wiped clean from the record when a taxpayer passes away. In this post we’ll discuss the general process and give you some tips on how to navigate some of the difficult steps one may encounter.

The role of the executor of the estate. When a person dies, someone may apply to the court requesting that they be allowed to settle the estate. This person could be an heir or the executor of the estate, and is referred to as the estate administrator. Once they have officially been appointed by the probate court, Letters Testamentary are issued to authorize them to act on behalf of the deceased. The estate administrator is responsible for collecting all of the deceased’s assets such as cash, bank accounts, investment accounts, personal property and titles to real estate. They then will ensure that all creditors are paid and then distribute the remaining assets to the heirs.

For example, if you are the estate administrator when your father or mother passes away, you can’t simply distribute their assets to the people named in the will immediately. First, you need to pay off any debts your parent owed at the time they died. If that parent owed taxes to the IRS, they will be included in the debts that must be paid.

Income generated before and after date of death. Sometimes, loved ones may be confused as to what must be included on which tax return. Here, we hope to add some clarity. Income earned up through the date of passing is included on the taxpayers final Form 1040. Any income generated after the day of death is earned by the deceased’s estate.

Filing of tax returns. The estate administrator is the person who is responsible for ensuring that all income tax returns for the deceased have been filed. This includes the final income tax return for the year of death. In this post on our sister site, we discuss how to file a deceased persons tax return.

To find out whether the deceased filed all income tax returns before his death, the estate administrator will have to look through the deceased’s personal records. They can also request information from the IRS to not only check return status, but get missing data (i.e. W2s, 1099s, 1098s, etc) needed to file returns. Check this page on the IRS’ website to learn more and request data.

If the estate earns money that is taxable, either from interest, dividends or rental income, these taxes are paid from the estate. According to the IRS, an estate administrator must file an income tax return for an estate if its assets generate more than $600 in income per year. This is done via IRS Form 1041.

IRS taxes owed at date of death. After you review the deceased’s personal papers and correspondence or you file any outstanding income tax returns, you may discover that your loved one still owes taxes to the IRS. A public records search may reveal that the IRS has already filed a Notice of Federal Tax Lien against the deceased’s home, vacation property, car or other property. The tax lien is official notice that the deceased owes back taxes. The outstanding amount will be deducted from the proceeds of their remaining assets to pay their taxes.

Do relatives have to settle unpaid taxes with personal funds? When a decedent’s assets are insufficient to cover his/her federal income and gift tax liabilities, relatives are generally not responsible for the remaining balances. However, there are some exceptions to this. There are payment obligations for the following individuals when tackling a decedent’s debt:

- Anyone who co-signed for a loan with the decedent,

- Anyone who was a joint account holder with the decedent,

- Spouses in the community property states of Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington and Wisconsin. Community property from a marriage can be put toward debt obligations, but spouses aren’t responsible for debts that predate the marriage.

- Residents of states where law requires a surviving spouse to pay off some of the debts—namely health care expenses, and

- Anyone who shares in any debt of the decedent

Additionally, an executor could be held personally accountable for the tax bill if:

- The executor distributes assets to heirs and beneficiaries before paying the taxes,

- The executor pays off other debts of the estate before paying the tax liabilities, or

- The executor is aware of the insufficient funds and inability to pay the taxes and spends the assets otherwise.

If you still need more information on this topic, feel free to see the Deceased Persons – Probate, Filing Estate and Individual Returns, Paying Taxes Due page at the IRS’ website.

Can the IRS Seize My Car?

You may have heard about the IRS seizing a taxpayers assets for unpaid taxes. These can include, among other things, the vehicles that they own. So the short answer to the question is yes, the IRS can seize a taxpayers vehicle. But let’s discuss the mechanics of how it gets to this point and some other important items shall we?

Why does the IRS seize vehicles? The first thing to know is that if you owe the IRS under $5000, your assets may not necessarily be seized and sold off. Per the 2019 IRS Data Book, in 2018 and 2019 the IRS seized a total of 275 and 228 assets respectively. Also, if you lease property, then you aren’t the legal owner. The IRS can’t seize items you don’t own, unless you have built up equity, or an ownership interest, in a leased asset. For most items, such as a rented auto, you won’t have any equity or it will be too small for the IRS to consider.

In the instances above, the IRS will seek to satisfy the collection of the debt owed through other means. This could include garnishing your income or seizing your federal tax refund. Now if the debt is substantial, then that’s where vehicle seizure comes into play.

The IRS utilizes progressively serious methods to try to collect your tax debt before seizing your vehicle. It will begin by informing you of your tax debt and giving you the opportunity to pay it. When they have sent numerous notices and attempted to collect, but have been unable to or can’t communicate with you regarding a reasonable plan for repaying your debt, it will proceed to file a federal tax lien against you. The Notice of Federal Tax Lien will alert creditors that the government has a legal right to your property.

Once other methods of collection have been exhausted, the IRS will use its power to seize assets by use of a levy. An IRS levy permits the legal seizure of your property to satisfy a tax debt.

How does the IRS seize a vehicle? A typical IRS seizure usually goes as follows:

- Local law enforcement accompanies IRS Revenue Officers so they are not interfered with nor attacked.

- The Revenue Officers will present their credentials to the taxpayer as well as the order (typically from a judge) that states they have a right to take the property.

- The IRS contractors (e.g. towing companies) will then secure the asset and remove it from the property for storage at a IRS facility.

We scoured the internet for a video showing an actual IRS vehicle seizure in process. This very dated video is all we could come up with. Regardless of how old it is, note how high the tension is!

What does the IRS do with the seized vehicles? The first thing that happens is that the vehicle gets moved to a storage facility. Next, the taxpayer is usually given one last attempt to settle the debt and reclaim the asset. But simultaneously, the IRS post public notice that the item is available for purchase from the US Government.

Generally speaking, the vehicle will be sold off relatively quickly, usually at an auction that is open to the public. The money raised from the sale is then applied to the tax debt that you owe to the IRS. The goal of seizing assets is to satisfy the debt as quickly as possible since you failed to pay it off yourself.

The image below shows seized vehicles by the IRS and how they notify the public of an auction. Anyone want to purchase a 2018 Ferrari??

How to avoid seizure. The best way to avoid having your assets seized is to file your taxes and pay what you owe on time each year. However, if you cannot fulfill either of these obligations, you should communicate with the IRS and be honest about your financial situation.

You could be eligible for a payment arrangement, which would allow you to pay off your debt in monthly payments. The arrangement will take into consideration:

- How much money you make

- Your household size

- How much you pay in rent, utilities, and other basic expenses

- The total value of your assets

The IRS will then determine a monthly amount that you should be able to pay toward your debt. In extraordinary situations, your tax debt could be forgiven. Forgiving a tax debt is a rare occurrence. However, it could be possible if you experience hardships like:

- High medical costs

- Divorce

- Death of an immediate family member

- Terminal illness

- Job loss

- Slowing down of your business

Click above to watch our Money Management and Tax Chit Chat video series!

Click Above For Your Top Secret Guide To Tax Reduction, Business Success and Solving IRS Debt Problems!

Click Above To Learn 111 Ways To Slash Your Tax Bill!